Choosing between buying a plot of land and buying a ready house is one of the most important real estate decisions you will make. The right choice depends on your financial goals, timeline, risk appetite, and lifestyle needs.

Both options offer advantages. Both come with trade-offs. The key is understanding how they differ in terms of cost, appreciation, flexibility, and long-term returns.

A plot is undeveloped residential land. When you purchase it, you are buying only the land, not a structure.

That means you control what gets built and when.

Construction Responsibility

You must hire architects, contractors, and manage the entire home construction process. This includes approvals, materials, supervision, and budgeting.

Timeline to Build

Construction can take anywhere from 8 months to 24 months depending on scale and approvals. If you are not in a hurry, this flexibility works in your favor.

Legal Approvals Involved

Plot purchases require careful title verification, zoning clearance, encumbrance checks, and building plan approval. Legal due diligence is critical in land investment.

Buying land offers freedom, but it requires planning and patience.

Buying a house typically means purchasing either:

Ready-to-Move vs Under-Construction

A ready house allows immediate possession. An under-construction property may be slightly cheaper but involves delivery risk.

Immediate Usability

You can move in or generate rental income immediately.

Builder Involvement

The developer handles construction quality, approvals, and infrastructure. However, builder credibility is important.

Ownership Structure

Buying a house prioritizes convenience over customization.

| Factor | Buying a Plot | Buying a House |

| Initial Cost | Lower upfront cost | Higher purchase price |

| Loan Availability | Limited, stricter terms | Easier home loan approval |

| Appreciation Potential | High land appreciation | Moderate (structure depreciates) |

| Customization | Full design freedom | Limited structural changes |

| Rental Income | Not possible until built | Immediate rental yield |

| Maintenance Cost | Minimal initially | Ongoing repairs & upkeep |

| Risk Level | Legal & development risk | Builder & aging risk |

| Liquidity | Slower in some areas | Higher in urban markets |

For Plots

While the land cost may be lower, total project cost can exceed expectations.

For Houses

Over time, maintenance costs reduce net returns.

Land Appreciation Trends

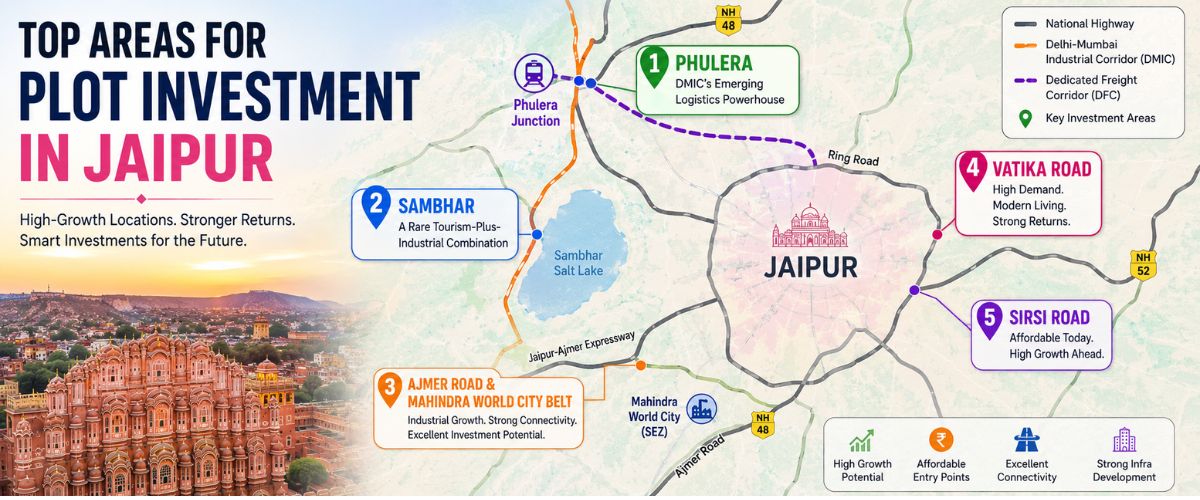

Land typically appreciates faster than constructed property, especially in infrastructure growth corridors and developing suburbs.

Structure Depreciation

The building portion depreciates due to wear and tear. After 15–20 years, renovation becomes necessary.

Location Impact

Location drives property value. A plot in a future growth zone may outperform a flat in a saturated area.

Demand Cycles

Apartments sell faster in metro cities. Plots perform better for long-term capital appreciation.

If your focus is pure investment return, land often delivers stronger percentage growth over 10+ years.

Loan-to-Value Ratio

Plot loans usually have lower LTV ratios compared to home loans.

Interest Rates

Interest rates for land loans are often slightly higher.

Tenure Flexibility

Home loans may extend up to 30 years. Plot loans often have shorter tenure unless combined with construction financing.

Construction Loan Process

Funds are disbursed in stages based on project progress.

Financing is generally smoother when buying a house.

Time Commitment: Are You Ready to Manage Construction?

Building a home requires:

If you have limited time, construction can become stressful.

Customization vs Convenience

With a plot, you design everything — layout, elevation, ventilation, expansion possibilities.

With a house, you trade customization for immediate comfort and convenience.

It comes down to control versus simplicity.

Title Verification Risks

Plot purchase demands thorough legal checks to avoid disputes.

Builder Credibility Risks

Delays and quality issues can affect under-construction homes.

Market Liquidity

Urban houses are easier to resell. Plots may take longer but offer higher appreciation.

Infrastructure Uncertainty

Land value depends heavily on future development plans.

In metro cities, ready homes often offer better liquidity and rental yield.

In developing suburban zones, plots usually see stronger land appreciation due to infrastructure expansion.

Location strategy can completely change your investment outcome.

Over 10 years:

If your priority is wealth creation through appreciation, plots often win.

If your goal is stable income and utility, houses make more sense.

Real estate rewards planning, not impulse decisions.

Smart for living: Buy a ready house.

Smart for rental income: Buy a house in a prime location.

Smart for long-term investment: Buy a well-located residential plot.

Smart for flexibility: Choose land and build when ready.

There is no universal winner. The smarter move is the one aligned with your financial strategy and life stage.

Is buying land a better investment than buying a house?

For long-term capital appreciation, land often performs better, especially in growth areas.

Which is easier to resell?

Houses in established urban locations generally sell faster.

Can I get a full loan for a plot?

Usually not. Banks offer lower funding compared to home loans.

Does a house lose value over time?

Yes, the structure depreciates, but the land underneath typically appreciates.

What is safer legally?

Both are safe if proper legal due diligence and documentation checks are completed.