What Is Khata and Why It Matters Before Buying a Plot?

If you are planning to buy a residential plot that follows the Khata system, one document that will come up in almost every conversation is the Khata certificate. Most buyers have heard the word, few understand what it actually means, and even fewer know the difference between an A Khata and a B Khata before they sign the agreement.

This is especially relevant if you are exploring a farmland project near Bangalore, where land records often involve both BBMP and Panchayat jurisdictions. Understanding Khata before you invest can save you from costly surprises later.

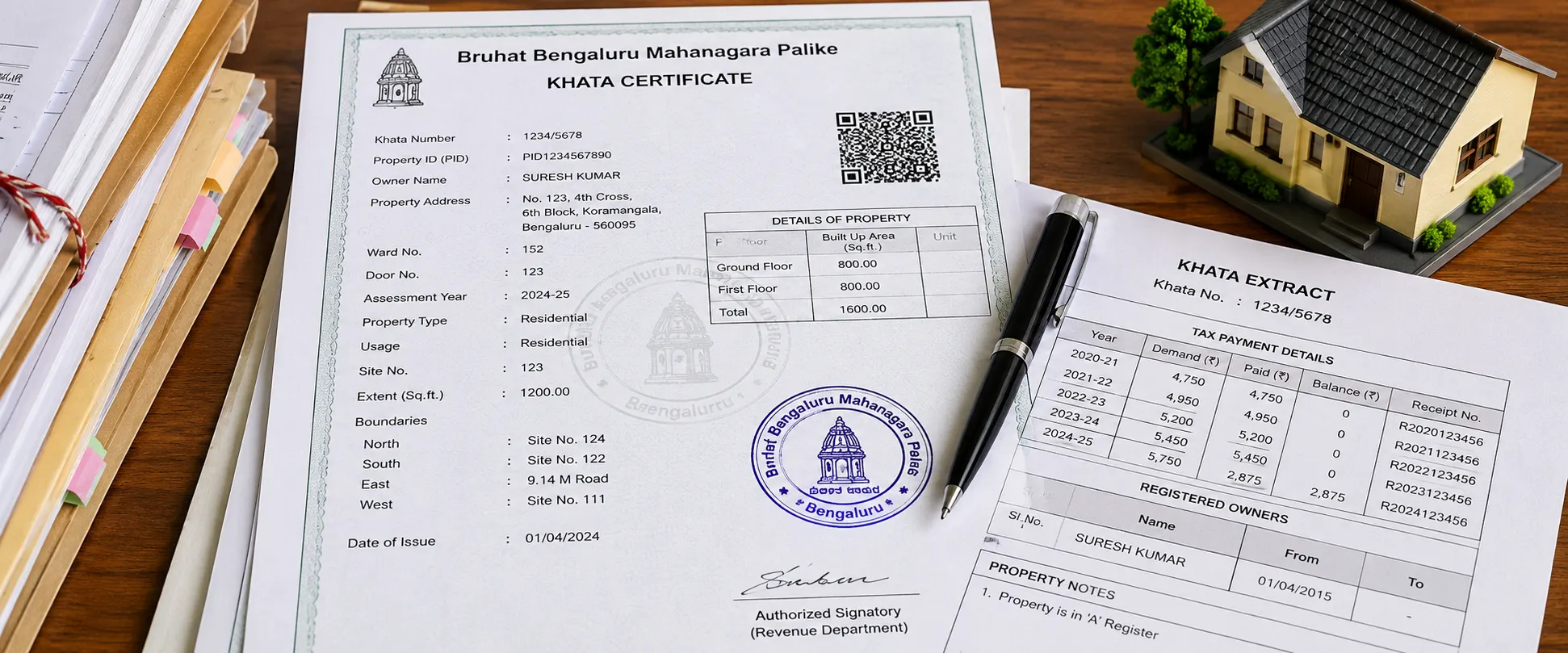

What Is a Khata Certificate?

A Khata is an account entry maintained by the local municipal authority, such as BBMP in Bengaluru, that records a property owner's details for the purpose of property tax assessment. The word Khata literally means account in Kannada and several other Indian languages.

It is not a title document and does not prove ownership on its own, but it is an official acknowledgment by the local body that a particular person is liable to pay property tax on a specific property.

Many buyers confuse Khata with a title deed or a sale deed. The sale deed is the document that transfers ownership from the seller to the buyer. The Khata is separate and comes after registration.

The Khata Certificate Includes:

Owner's name

Property address

Plot size

Property Identification Number (PID)

Annual tax assessment details

The Khata Extract Contains:

Tax payment history

Outstanding dues

Ownership changes

Property records history

Why a Valid Khata Is Important?

Building plan approval may not be possible

Water and sewage connections may be denied

Banks may refuse loans

Future resale may become difficult

A Khata vs B Khata: What Is the Difference?

The most important distinction in the Khata system is between A Khata and B Khata.

A Khata:

An A Khata is issued for properties that are:

Legally approved

Fully compliant

Located in approved layouts

Free from pending dues

Eligible for building approvals and loans

B Khata:

A B Khata is maintained for properties that may have:

Unapproved layouts

Revenue land issues

Pending regularization

Planning authority approval problems

Betterment charge issues

Paying property tax on a B Khata property does not make the property legal.

A Khata vs B Khata Comparison:

Feature

A Khata

B Khata

Legal Status

Fully compliant and approved

Non-compliant or pending regularization

Building Plan Sanction

Allowed

Not permitted

Bank Loans

Available from most banks

Often denied

Property Tax Records

A Register

B Register

Utility Connections

Allowed

Often restricted

Resale Value

Higher

Lower

Conversion Required

No

May require conversion

Questions to Ask Before Buying

Is the property A Khata or B Khata?

Is the layout approved?

Have betterment charges been paid?

Can the property obtain building approval immediately?

How to Transfer a Khata After Buying a Plot

Khata transfer should be completed shortly after registration.

Documents Required:

Registered sale deed

Previous owner's Khata certificate

Khata extract

Latest tax paid receipt

Encumbrance Certificate (13 years)

Aadhaar Card

PAN Card

Property sketch or site plan

Possession letter (if applicable)

Betterment charge receipt (if applicable)

Self-declaration form

Transfer Process:

Submit application at BBMP Citizen Service Centre.

Submit required documents.

Site inspection by BBMP officials.

Verification of records.

Issue of new Khata certificate.

Typical processing time: 30–90 days.

What Is Khata Bifurcation?

Khata bifurcation means splitting one Khata into multiple Khatas.

Example: A 4,000 sq ft property is divided into two 2,000 sq ft plots. Each plot requires a separate Khata.

When Is It Required?

Layout developments

Property subdivision

Sale of portions of larger land parcels

Documents Needed

Original Khata

Approved layout plan

Sale deed

Surveyor certificate

Property boundary details

Buyer Checklist

Has Khata bifurcation already been completed?

Am I receiving an independent Khata?

Is my plot linked to a parent Khata?

How Does Khata Affect Your Ability to Get a Plot Loan?

Banks review Khata documents during legal verification.

A Khata Properties

Generally eligible for:

Plot loans

Home loans

Construction loans

B Khata Properties

Often face:

Loan rejection

Lower loan eligibility

Additional legal scrutiny

Documents banks typically require:

Khata certificate

Khata extract

Tax receipts

Encumbrance Certificate

Khata status directly impacts future resale value and financing options.

How to Verify Khata Details Before Buying

Online Verification

Verify through BBMP records using:

Property ID

Owner name

Application number

Check:

A or B Register status

Outstanding dues

Property notes or restrictions

Offline Verification:

Review:

Original Khata certificate

Khata extract

Tax payment history

Visit the BBMP ward office to verify:

Property records

Dues

Encroachments

Ownership details

Verification Checklist

Check BBMP online records.

Confirm A or B Khata status.

Examine original documents.

Match ownership records.

Verify tax dues.

Visit ward office.

Verify parent Khata for layout plots.

Confirm issuing authority.

Cross-check with Encumbrance Certificate.

Key Takeaways

A Khata is a municipal record, not a title document.

A Khata properties are eligible for approvals and loans.

B Khata properties carry legal and financing risks.

Verify BBMP Khata or Panchayat Khata status before purchase.

Complete Khata transfer immediately after registration.

Ensure Khata bifurcation is completed for layout plots.

Verify records both online and at the ward office.